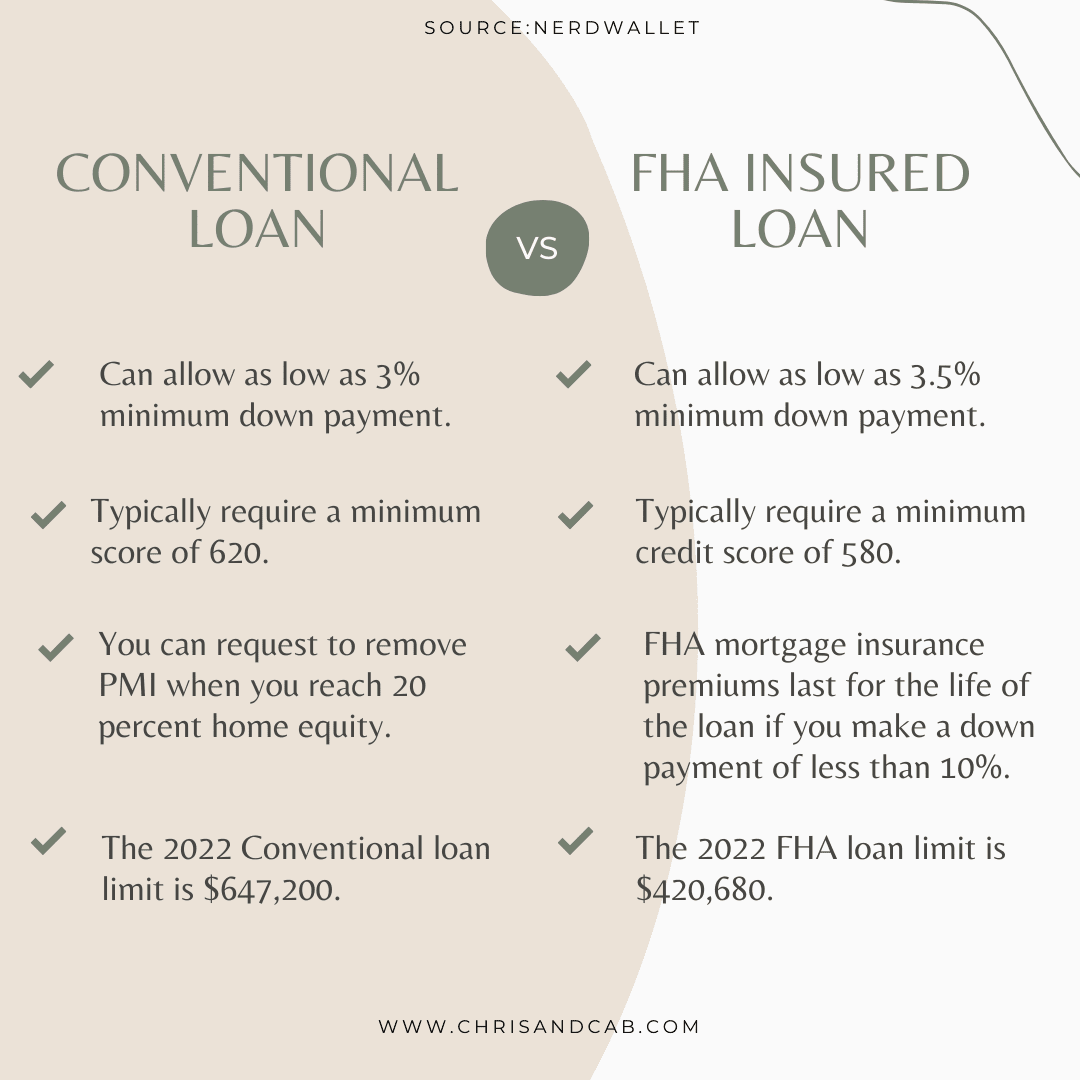

The TLDR is that FHA loans are insured by the Federal Housing Administration, while Conventional loans aren’t insured by a federal agency. Therefore, criteria to qualify for an FHA loan is less stringent, and it’s typically easier to qualify for an FHA loan.

You can qualify for an FHA loan even if your credit score is in the lower 500s if you can put at least 10% down. If your credit score is at least 580, the minimum down payment required by FHA loans is only 3.5%.

In comparison, most conventional loans require a credit score of at least 620 to qualify. Conventional loans also allow low down payments, as little as 3% down.

You’re probably asking, which has lower interest rates, FHA or Conventional? Conventional rates are typically a little higher than FHA mortgage rates. But mortgage insurance could me higher or lower than FHA insurance rates (it just depends).

If you’re asking should you go Conventional or FHA, the TLDR of our opinion is that you should go Conventional if you can because the PMI is easier to get rid of. but if FHA is all that you can qualify for, that shouldn’t deter you from purchasing a home and experiencing the benefits of home ownership.